The BEAD program begins to bear fruit

Washington, DC (January 16, 2025) - On January 13, 2025, the NTIA announced its approval of Louisiana’s BEAD Final Proposal. Delaware’s approval followed the next day. With those two landmarks, coming as the fourth year since the passage of the Infrastructure Investment and Jobs Act (IIJA) begins to elapse, the BEAD program is at last beginning to bear fruit.

As Louisiana and Delaware move toward signing contracts with subgrantee Internet Service Providers (ISPs), who should then initiate the construction of networks, one more state Final Proposal, Nevada’s, is being reviewed. Most states are well behind these frontrunners and are just getting started with subgrantee selection.

But once BEAD network construction begins, it will only accelerate, probably hitting its stride in 2026 and 2027.

For ISPs interested in contributing to the nationwide BEAD solution by expanding their coverage with its subsidies, now is prime time for preparing and submitting projects. Some states’ application windows have closed, but in most states, opportunities are still open now or will open up soon.

The process is a little different in each state, particularly with respect to what areas are open for bid. Most, but not all, states predefine project areas in some way, and those that do vary greatly in the size of the predefined areas and in whether and how they can be bundled.

The BEAD program launched in 2021 with the ambitious goal of universal broadband coverage. Will it achieve it? Yes and no.

If you count low-Earth orbit (LEO) satellite service, such as that currently offered by Starlink and promised by Amazon Kuiper, a certain kind of universal broadband coverage has already been achieved without any help from BEAD. BEAD funds will mostly support a lot of new fiber coverage in areas where LEO satellite and maybe some unlicensed fixed wireless are currently the only options. But where “reliable” — fiber, cable, and licensed fixed wireless — projects are not forthcoming, BEAD will often turn to LEO satellite as the solution of last resort.

BEAD has also begun to spin off funds for uses other than last-mile broadband deployment. Louisiana’s Final Proposal describes over $500 million of BEAD non-deployment spending, while Delaware required only $17 million of $107 million for last-mile deployment. At the same time, Nevada, which had to supplement its BEAD allocation with $94 million in other federal funding to meet the universal coverage goal, may be a harbinger of BEAD funding shortfalls in other states. Despite the complexities, the BEAD program appears to be on its way to impressive, if messy, success.

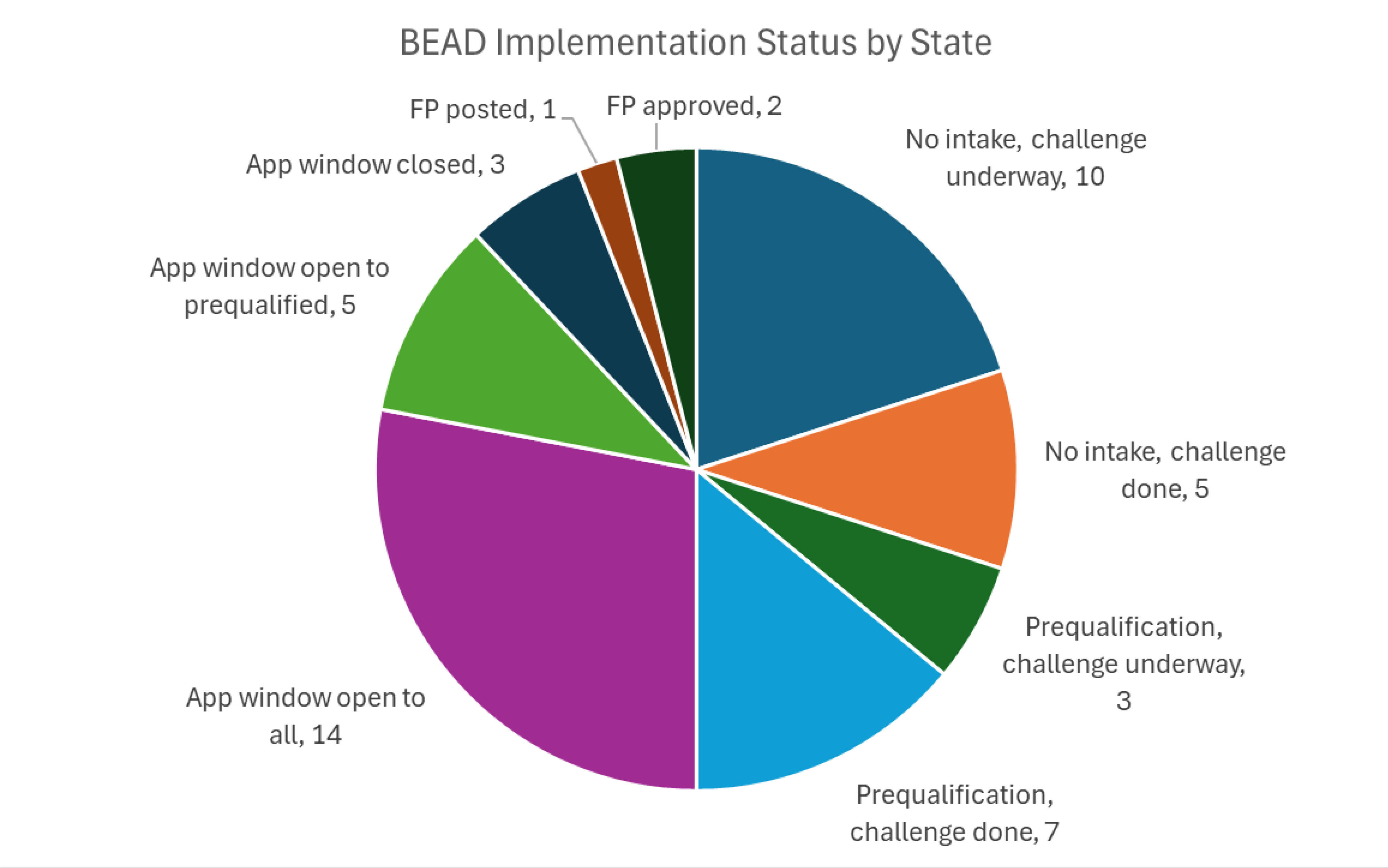

Here's where states are in the BEAD process.

All states got their BEAD Initial Proposals approved by the end of 2024, but beyond that, different states are at different stages, as shown in Figure 1 below. Most states have completed the challenge process, but 13 are still working toward that goal. Similarly, there are 15 states that are not yet accepting any application materials from ISPs. Some states are accepting prequalification materials while still working through the challenge process. Only a minority of states have gotten as far as accepting project applications.

At the time of writing, Connected Nation (CN) identified 19 states with open (or very soon to open) application windows. Most have well-defined closing dates. A few of those states are only accepting projects from applicants who have already been vetted in prequalification (various called “letter of intent,” “prequalification,” and “preapplication”) rounds that have already closed. Most, however, are open to all applicants.

Louisiana’s Final Proposal approval process seems to have gone smoothly. Although the approved Final Proposal includes a summary of the many public comments it received, “ConnectLA thoroughly analyzed the comments and concluded that no significant changes to the Final Proposal were necessary.” There also appears to have been little or no NTIA curing required for Louisiana’s Final Proposal, in contrast to extensive curing for most states at the Initial Proposal stage. At the time of writing, Delaware has not posted its approved Final Proposal.

Colorado and Kansas have closed their application windows, though Colorado will be opening a Round 2 application window on January 27. Several more application windows will be closing soon, as shown in Table 1:

Many application windows are closing soon.

|

State |

Application window close date |

Link |

|

PA |

21-Jan |

https://www.broadband.pa.gov/broadband-equity-access-and-deployment-bead-program/ |

|

WY |

24-Jan |

|

|

HI |

31-Jan |

|

|

WA |

31-Jan |

|

|

AZ |

5-Feb |

|

|

NH |

5-Feb |

https://www.nheconomy.com/office-of-broadband-initiatives/bead/subgrantee-selection |

|

NY |

7-Feb |

|

|

IN |

12-Feb |

|

|

MO |

20-Feb |

https://ded.mo.gov/programs/community/broadband-equity-access-and-deployment-bead-program |

|

WI |

25-Feb |

https://psc.wi.gov/Pages/ServiceType/Broadband/GrantBEAD.aspx |

|

ME |

27-Feb |

|

|

VA |

1-Mar |

|

|

KY |

16-Mar |

https://broadband.ky.gov/BEAD/Pages/Subgrantee-Selection.aspx |

|

MI |

9-Apr |

|

|

AK |

14-Apr |

https://www.commerce.alaska.gov/web/abo/AlaskaBroadbandGrantProgram.aspx |

Among states with open application windows, Hawaii only accepts applications that propose to reach all the unserved and underserved BSLs in entire counties, while Arizona, Washington, Missouri, and Maine have posted maps of custom predefined project areas that they will require applicants to propose to serve.

Missouri’s project areas were designed on the basis of industry input. At the other extreme, North Dakota lets applicants propose any set of BEAD-eligible locations they wish to. In between are states that use, as the required units of which project areas should be comprised, pre-existing geographies such as census block groups (Pennsylvania), ZIP Code tabulation areas (Virginia), or census blocks (Indiana).

It will be a few more weeks before any more Final Proposals come due, although they could appear sooner: Delaware and Nevada both posted Final Proposals well in advance of the deadline. Upcoming state deadlines for Final Proposal submission to the NTIA are:

- April 2025 — Kansas and West Virginia

- May 2025 — Washington, D.C., and Pennsylvania

- June 2025 — Colorado, New Hampshire, Illinois, Oregon, Kentucky, and Maine

Final Proposals should be posted for public comment a few weeks before they are due to the NTIA so that states can complete the 14-day public comment period and integrate feedback.

Nevada’s BEAD funds weren’t enough, so it had to supplement them with SLFRF, and its solution is still 11% reliant on LEO satellite.

The three Final Proposals that have been posted exhibit one particularly striking contrast. Two of the states — Louisiana and Delaware — had easily enough funds to achieve the BEAD goal of universal coverage. By contrast, Nevada, didn’t have enough BEAD funds to deliver service to the whole state and had to supplement it with State and Local Fiscal Recovery Funds (SLFRF) from the American Rescue Plan Act (ARPA) to reach all its unserved and underserved broadband serviceable locations (BSLs). Why the difference?

Delaware began the BEAD process with very small coverage gaps of just a few thousand BSLs. Like other states with small coverage gaps, it benefited from the fact that the IIJA set a floor of $100 million under state BEAD allocations. As a result, Delaware’s BEAD allocation per BSL was high. It didn’t need it. Delaware got all its BEAD-eligible BSLs served with 100% end-to-end fiber at a cost of just over $3,000 per BSL.

All the BEAD funding in Delaware went to one company, Verizon, which committed to deploy to 4,674 locations in return for $17,443,624 in subsidies. But Verizon did not capture all the BSLs — 18.2% of the BSLs were awarded to Comcast, which is apparently willing to make a commitment to build to them without any subsidy. It may seem odd that Comcast would accept such unfunded obligations, but presumably the company wanted to deploy to the locations anyway, could build using its own funds and simply wanted to avoid facing a subsidized competitor.

With only $17.4 million of its $107.7 million BEAD allocation needed for last-mile deployment to achieve universal coverage, Delaware can spend the vast majority of its BEAD dollars on non-deployment uses.

Louisiana, as previously explained in a previous blog post (see “How Louisiana Solved the BEAD Rubik’s Cube”), also achieved universal broadband coverage with over $500 million in funds to spare, and the state plans to work with several other state agencies and stand up a variety of programs to make use of the remaining funds. With far larger coverage gaps and a more rural geography than Delaware, Louisiana had to spend more per BSL than Delaware — $5,355 — and far more in total — $748 million — and its fiber share was slightly lower at 95%, but funding was ample.

Nevada had different rules from Louisiana and Delaware. For example, it didn’t allow applicants to bundle project areas. But the main factor driving its higher costs is surely Nevada’s geography and terrain, with more mountains and far lower population densities than the two states further east.

Of Nevada’s 995 project areas, 340 contained just one single BSL. Another 165 contained only two. These tiny project areas were overwhelmingly awarded to the LEO satellite service that is being launched by Amazon Kuiper. Amazon’s LEO projects also dominated project areas with three to five BSLs (85%) and six to 10 BSLs (70%). Only in project areas with 21 or more BSLs did Amazon’s share fall below half.

Altogether, Amazon won 782 of the 995 project areas, but since these were mostly small, it captured only 11% of all BSLs and only 3% of Nevada’s BEAD funds, since Amazon showed a willingness to commit its capacity to remote Nevada BSLs on a very affordable basis. Amazon projects that it will offer speeds of 150 Mbps download, 20 Mbps upload to all its Nevada BEAD locations.

Fixed wireless also has a small footprint in Nevada’s BEAD solution, with just over 5% of BSLs spread across project area sizes, but with the largest market share (14.5%) in areas with 51 to 100 BSLs. In the largest project areas, fixed wireless’s market share was tiny (4.9%) but larger than that of LEO satellite (3.9%). The majority of projects will use cellular spectrum. Most of the fixed wireless awards will go to Hot Spot Broadband and Welink Communications.

Although fixed wireless will have a smaller BEAD footprint in Nevada than LEO satellite, it will capture more funding, with over $57 million, compared with LEO satellite’s $14.5 million. Per BSL, LEO satellite required by far the least subsidy funding at under $3,000 per location, while fixed wireless required the most subsidies at over $24,000 per location. But Nevada’s fixed wireless BEAD winners also project much faster speeds, far above the 100/20 baseline in all cases and often gigabit symmetric. These speeds are far faster than all but a tiny fraction of the fixed wireless coverage shown in the FCC National Broadband Map.

As in Louisiana and Delaware, end-to-end fiber projects captured a large majority of the BSLs (83%) and the funding (84%) in the Nevada BEAD program. Compared to LEO satellite and fixed wireless, fiber had a lot of winners, with 14 different companies winning BEAD funds for fiber expansion, although 80% of the BSLs went to just three ISPs: Stimulus Technologies of Nevada (46% of fiber BSLs), Hot Spot Broadband (20% of fiber BSLs), and Commnet of Nevada (14%).

Stimulus Technologies and Hot Spot Broadband were the biggest BEAD winners, with $143 million and $139 million, respectively. Stimulus won almost exclusively fiber awards, while Hot Spot won mostly fiber plus just over 1,000 fixed wireless BSLs. These two companies won just over half of Nevada’s $489 million subsidy spend from BEAD and SLFRF.

In part, Nevada found it challenging to achieve universal coverage because its BEAD allocation per post-challenge eligible BSL— $416 million in total BEAD funding divided by 44,214 eligible BSLs — was just $9,424, much less than $18,853 in Delaware, and slightly less than $9,704 in Louisiana, where the population density is higher and the terrain is more friendly to deployment. Western states like Alaska, Wyoming, Montana, New Mexico, and Idaho resemble Nevada in their low population densities and mountainous terrains.

The challenge process has generally reduced BEAD’s footprint and improved its funding outlook, but it varies.

Another important factor affecting the sufficiency of BEAD funding is the challenge process. All states were required to run a challenge process to check the accuracy of the FCC maps before launching BEAD subgrantee selection. Although the current FCC maps are more granular than ever, they are still based on ISP self-reported data, which some have suggested overstates their actual coverage. Other components of BEAD eligibility determination, such as the footprint of existing federally subsidized deployment obligations, which BEAD is not supposed to overbuild, were also subject to correction as part of the challenge process.

Importantly, too, most states chose to allow “planned service challenges” by ISPs that, while not yet serving an area, were in the process of deploying to it and would complete deployment long before a BEAD subgrantee ISP could be expected to do so. In such cases, it’s reasonable to remove the area from BEAD eligibility. Planned service challenges were important in some states and resulted in the removal of many BSLs from the lists.

With these different elements in the challenge process, it was possible for a state’s BEAD footprint to change in either direction, leaving it with either more or fewer BEAD-eligible BSLs in need of projects than the state had anticipated when it submitted its Initial Proposal.

Kansas is a state where the challenge process reduced the BEAD footprint and made the challenge of achieving universal broadband coverage easier. The latest FCC data find 38,113 underserved and 46,799 unserved BSLs in the state, with some covered by previous programs. But after the challenge process, Kansas found that it was left with only 21,571 underserved and 30,772 unserved BEAD-eligible BSLs, leaving over $8,000 in BEAD funding per BSL and a much higher likelihood that the state can achieve universal broadband coverage with funds to spare.

Louisiana and Delaware both had fewer BEAD-eligible BSLs than the number of unserved and underserved units in the FCC maps, which helped them achieve universal coverage with funds to spare.

By contrast, Nevada’s 44,214 BEAD-eligible BSLs considerably exceed the 21,265 unserved and 5,341 underserved units that are identified in the FCC maps. Other states with more BEAD-eligible BSLs than the unserved and underserved units displayed in the FCC maps include Colorado and Arizona.

The NTIA’s new alternative technology guidance clarifies the role of unlicensed fixed wireless and LEO satellite, though still leaving states with flexibility on implementation.

Nevada’s experience, and the steep economic challenge that the BEAD program faces in some states, underscore the need for alternative, usually lower-cost technologies like unlicensed fixed wireless and LEO satellite in closing broadband coverage gaps in the hardest-to-serve places and achieving the BEAD program’s universal service goal.

That makes NTIA’s January 2 release of new “Final Guidance for BEAD Funding of Alternative Broadband Technology” timely. The guidance was released in pre-decisional form during summer 2024 and seems to have influenced states’ alternative technology plans already, but it underwent significant change in the wake of a public comment period.

The guidance includes an important win for unlicensed fixed wireless, which has hitherto been sidelined as BEAD sought to secure coverage by “reliable” broadband technologies that were defined in a way that excludes it. The new guidance doesn’t change the fact that wherever the only existing 100/20, low-latency coverage is provided by unlicensed fixed wireless, BEAD will make the affected locations eligible for subsidies to deploy new coverage using reliable technology.

If no reliable technology projects materialize, however, the new guidance adds a step to the process, whereby the state broadband office will consult the FCC National Broadband Map, see if there’s an unlicensed fixed wireless provider claiming coverage there and, if so, give that provider an opportunity to demonstrate that its coverage is adequate and should not be overbuilt by BEAD after all.

Where neither a BEAD-funded reliable technology project nor an existing unlicensed fixed wireless provider meets the need, the last resort for the BEAD program will be to seek to fund an alternative technology project. If the pattern observed in Louisiana and Nevada continues, this will generally mean LEO satellite.

And the guidance indicates that “LEO Capacity Subgrants” should be designed. These subgrants will not be tied to any specific new infrastructure. It doesn’t make sense for BEAD to fund new LEO satellites for specific locations, since it’s the nature of LEO satellite technology that the infrastructure (satellites) is in orbit, and satellites are constantly moving relative to the Earth’s surface, and handing off coverage from one to another. Instead, LEO Capacity Subgrants should “reserve capacity” locally provided by existing or future satellite fleets.

The guidance leaves some details to be worked out and indicates that the NTIA will provide additional technical assistance as states seek to operationalize it. But it makes it clearer than ever that, while BEAD will build a lot of fiber, if it succeeds in securing universal access to 100/20 broadband throughout the United States, it will do so by partnering with LEO satellite companies like Starlink and Amazon Kuiper.

Dr. Nathan Smith, Director, Economics and Policy

Meet the author

Dr. Nathan Smith monitors federal broadband policy, writes public comments for federal agencies that request advice on broadband policy implementation, and helps with business development and proposals